Introduction

This post aims to introduce the basic concepts related to bond, which will be used to understand the deeper concepts related to the bond market. In this topic review, we will start with understanding how significant role bonds play in the global capital market. Then we will see basic concepts like coupon, face value, covenant, indenture related to bonds, lastly, we will examine various types of bonds.

Role of Bonds in Global capital market

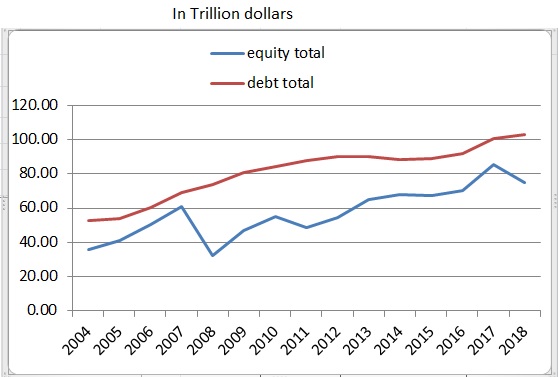

Bonds are the prominent source of raising capital by the borrower, and it far surpasses equity as a source of raising capital. The use of bonds as a source of capital over the year can be seen in the below image.

From the above data, we could see that in 2018 outstanding bond was valued at about $102 trillion far outstripping equity which stood at $74 trillion.

Various concepts related to bonds

Bonds are fixed income security which promises a fixed stream of cash flows to the bond holder in the form of a coupon at regular interval for a fixed period and face value at maturity.

Face value: Face value of the bond is the amount that issuer promises to pay once the bond matures. It is mentioned in the bonds contract. Face value is also called par value. It is important to note that the market value of a bond can be different from the face value depending on the prevailing interest rate in the market and return demanded by investors. We will discuss in detail the difference between the two in the next post.

Term to maturity: It refers to the length of time remaining for which the bondholder will receive regular payment and at the end of this period bond will mature, and the issuer will pay the face value and redeem the bond.

Coupon: Coupon is the regular cash or payment a bondholder receives. It is mostly annual or semiannual payment. The coupon is defined as a percentage of the face value of the bond, and the mentioned rate is in terms of per annum.

Let's take an example: A corporation wants to raise $1 million for 5 years. The corporation decides to raise this amount by issuing a bond with a par value of $1000 having 6% coupon paid semiannually for 5 years.

Now, Face value = $1000 (Note: This may or may not be market value)

Term to maturity = 5 years

coupon = 6%*1000 = $60

Note: Coupon mentioned above is an annual payment because the coupon rate is always mentioned annually. But, since issuer has promised to pay coupon semiannually, the investor will receive $30 every six months or (6%/2)*1000.

Bond Indenture: Bond is a contract between issuer and borrower, and as in any contract issuer and borrower has certain rights and obligation. All these right and obligations mentioned in the form of contract is called a bond indenture. The indenture also includes specific details related to bonds, like some bonds have call option attached to it.

Covenants: There is always a credit risk associated with bonds apart from bonds issued by the government in the domestic currency, which is almost credit risk-free. To protect the investor from these risks which may be credit risk or some other risk, certain provisions related to the borrower are included in the indenture. These provisions are called covenants.

There are basically two types of covenants:

Negative covenants: These provisions mention the action that borrower cannot take. Like taking further secured debt, selling the asset which has been pledged.

Affirmative covenants: These provisions mention the action that borrower needs to perform on its part. Like maintaining certain financial ration above the threshold, proper maintenance of pledged collateral.

Types of Bond

Apart from the bond whose example was given above, a straight bond, there are various other types of bonds as mentioned below.

Zero-coupon bond: These bonds don't pay coupon, the interest earned on these bond is because these bonds are issued at a discount to face value. When the bond matures investor gets face value of the bond.

Let say a zero-coupon bond is issued at 10% per annum for 5 years having a face value of $1000.

Now since this bond will not pay any coupon and only $1000 at the end of 5th year, to earn 10% per annum, the bond will be issued at $620.92 to the investor.

Dual currency bond: These type of bond pays principal in one currency and interest in other currency. This type of bond is used to raise money in one currency and pay interest in other currency.

Like a bond issued in euro but pays interest in us dollars.

Currency option bond: These type of bond generally gives the investor an option to decide in which of the currency, generally among two currency choices, they want payment in. This option is both for coupon and principal.

Step-up notes: In this type of security coupon rate increase over the period at a given rate.

Domestic bond: These are the bond issued by the firm present in the same country where the bond is traded and denominated in the same country currency.

U.S firm issuing the bond denominated in U.S dollar and traded in the U.S bond market.

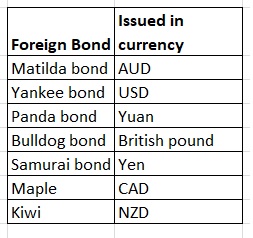

Foreign bond: These bonds are issued by the firm outside the country in whose currency the bond is denominated and traded in the market of denominated currency. The foreign bonds have unique names like samurai bond, it is the bond issued in Japan by a non-Japanese company.

Eurobond: These are the bond issue by a firm outside its domiciled country, and the bond is denominated in a currency different from both the home country of the firm or the country in which it is traded. Like a bond issued by Japanese firm is the U.S denominated in yuan.

Most of the Eurobonds are bearer bond, i.e. the ownership is with the person holding bond as it is not registered. It is important to understand that Eurobonds are not named in such a way because it was issued in Europe or denominated in euro.

Eurobond denominated in U.S dollar is called Eurodollar.

Deferred-coupon bond: These are the bond in which initial coupon payments are deferred for some time in future, the accrued coupon payments are paid at the end of the deferred period. The bonds are issued when certain project supporting the coupon payment are expected to generate cash flows in the future period.

Apart from these bonds, there are various other types of bonds which we learn about and understand as we move along our journey to understand fixed income securities.